TL;DR

California has made a significant shift in how estates can be handled. Under Assembly Bill 2016 California, the state raised the threshold for simplified probate of real property from $184,500 to $750,000, effective April 1, 2025. This change expands access to the small estate California process, allowing many families to avoid the time, cost, and complexity of full probate. For those reviewing an estate plan or managing a loved one’s assets, the implications are substantial. In this post, we will break down what changed, who now qualifies under the California small estate limit, and how the simplified probate California procedure actually works in practice.

What Assembly Bill 2016 (AB 2016) Actually Changed

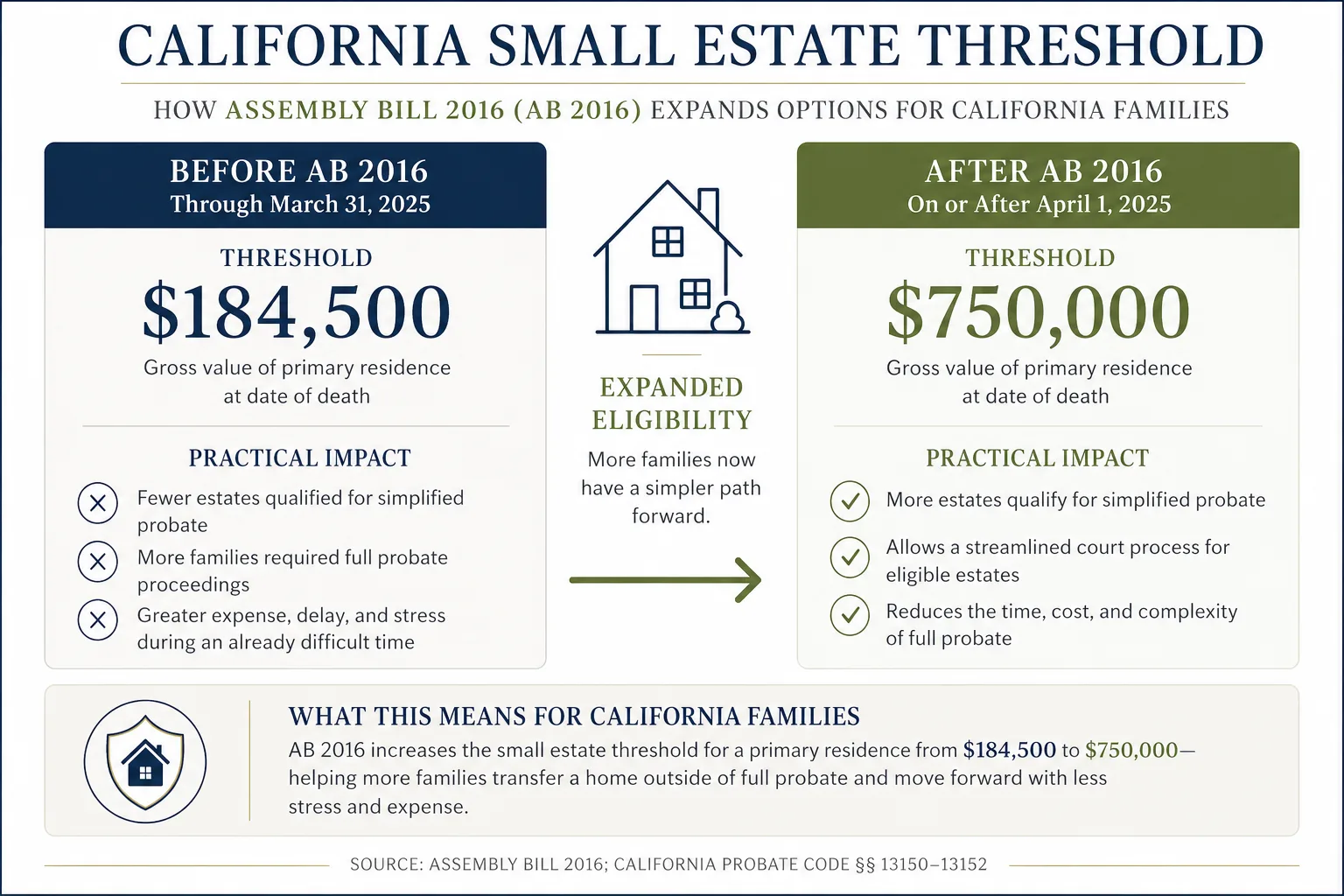

Assembly Bill 2016 California made a targeted but meaningful update to California’s small estate procedure. It raised the value limit for using a Petition to Determine Succession to Real Property under California Probate Code Section 13150 from $184,500 to $750,000.

This higher California small estate limit applies to deaths occurring on or after April 1, 2025. In addition, the law built in an automatic adjustment mechanism, requiring the threshold to be updated every three years to reflect inflation.

In practical terms, far more estates can now qualify for simplified probate California procedures when real property is involved, expanding access to a faster and more cost-effective alternative to full probate.

What the New Threshold Does Not Change

AB 2016 did not change every California small estate procedure. The personal property small estate affidavit under Probate Code § 13100 remains separate, with its own threshold, currently $208,850 for deaths on or after April 1, 2025.

That distinction matters. The general small estate affidavit and the real property petition are not the same tool. They have different requirements, different forms, and different limits. Families should not assume that qualifying under one procedure automatically means they qualify under the other.

Who Qualifies Under AB 2016 in California

To use the small estate procedure for California real property, the estate generally must meet these requirements:

- The decedent died on or after April 1, 2025.

- The qualifying California real property, generally the decedent’s primary residence, does not exceed $750,000 in gross value at the date of death.

- At least 40 days have passed since the date of death.

- No full probate proceeding is pending or has already been completed for the estate.

- The petitioner is a successor of the decedent, such as an heir, beneficiary, or trustee.

Under Assembly Bill 2016 California, the expanded California small estate limit applies specifically to a primary residence. Other types of real property, such as rental properties, vacant land, or commercial real estate, generally do not qualify under this simplified probate California procedure.

How the Procedure Works

The process is still a court procedure, but it is typically much more limited than full probate.

First, the real property must be appraised, usually through a probate referee. The petitioner then files a Petition to Determine Succession to Primary Residence, Form DE-310, with the probate court.

After filing, notice must be provided to the required heirs and beneficiaries. The court then holds a hearing, which is often brief if no one contests the petition. If approved, the court issues an order confirming the property’s transfer. That order is then recorded with the county recorder to complete the title transfer.

Realistic Timeline and Cost

Most petitions under this simplified probate California procedure are completed within 2 to 4 months from filing, assuming there are no complications. That is a meaningful reduction compared to the 9 to 18 months often required for full probate. Court costs and attorney fees are also significantly lower, since there is no full estate administration involved.

The Tradeoffs Many Families Do Not Consider

The expanded small estate procedure can save substantial time and money compared to full probate, but faster is not always simpler.

Once the court transfers title, the heirs become the owners of the property. That creates practical challenges that many families do not anticipate.

If multiple children inherit the home, every owner generally must participate in major decisions involving the property. Selling the home often requires signatures from all owners on listing agreements, purchase contracts, escrow documents, and deeds. The more heirs involved, the more complicated the process can become.

Problems frequently arise when one heir is living in the property, cannot be located, refuses to cooperate, or disagrees with the proposed sale. In those situations, transferring the property quickly through the small estate procedure may simply move the conflict to a later stage rather than eliminate it.

Transfers involving minor children can create additional complications. A minor cannot independently sell or convey real property. If a minor inherits an ownership interest, a later sale may require court involvement that the family was trying to avoid in the first place.

By contrast, a full probate administration places decision-making authority with the court-appointed personal representative, subject to court supervision when required. While probate is generally more expensive and time-consuming, it can provide a structured process for handling disagreements, selling property, and resolving occupancy issues that may be difficult once multiple heirs have already taken title.

In some situations, the small estate procedure is an excellent solution. In others, the long-term administrative challenges can outweigh the short-term savings. The best approach depends not only on the value of the property but also on the family dynamics and the likelihood that the property will need to be sold after the transfer.

When This Procedure Is Not the Right Tool

This process is not available or appropriate in every situation. It may not be the right fit if:

- The estate includes California real property valued above $750,000.

- There are contested heirs, will disputes, or creditor issues.

- The decedent owned real property outside of California.

- The property is already held in a trust, in which case the trust administration process should be used instead.

What This Means for Your Estate Plan

For established planners, this change meaningfully shifts how estate planning decisions are made. Many California families whose primary residence falls between $200,000 and $750,000 may now have a practical option to transfer that property using a simplified probate California procedure rather than defaulting to a full revocable trust. However, qualifying for the procedure does not necessarily mean it is the best choice. The number of heirs involved, the likelihood of a future sale, and whether family members are likely to cooperate can all affect whether the streamlined process ultimately saves time and expense. That does not mean trusts are unnecessary. Property can pass outside of probate in several ways depending on how assets are titled and structured, you can explore those options here: Property Without Probate. A trust still provides a level of control, privacy, and flexibility this process cannot match. Still, when the home is the only significant probate asset, a trust is no longer the automatic answer it once was. The right approach now depends more directly on your overall asset mix, your planning goals, and how comfortable you are with a limited court process.

Action Steps

- Confirm the property’s current value using a recent appraisal or a reliable comparable market analysis.

- Review your existing estate plan to determine whether the updated California small estate limit changes your strategy or reduces the need for a trust.

- If you are administering an estate where the death occurred on or after April 1, 2025, evaluate eligibility for the small estate procedure California process before opening full probate.

If you want clarity about how this applies to your situation, contact Randal P. Hannah Attorney at Law to schedule a free consultation. You can call our office directly or use the online form.

Frequently Asked Questions

What is the small estate threshold in California in 2025?

Under Assembly Bill 2016 California, the limit for using the Petition to Determine Succession to Real Property is $750,000 for deaths occurring on or after April 1, 2025. This applies specifically to qualifying California real property and is separate from the lower threshold that applies to personal property affidavits.

Does AB 2016 apply to deaths before April 1, 2025?

No. The updated California small estate limit only applies to individuals who passed away on or after April 1, 2025. Earlier deaths are subject to the prior threshold of $184,500.

Is the $750,000 threshold based on net or gross value?

The threshold is based on the gross fair market value of the real property at the date of death, not the equity after subtracting mortgages or other liens.

Do I still need a trust if my home is worth less than $750,000?

Not necessarily. Some families may reasonably rely on the simplified probate California process instead of creating a trust if the home is their only significant asset. However, trusts still provide advantages such as avoiding court involvement, maintaining privacy, and planning for incapacity, so the right decision depends on your overall estate plan and goals.

Not all assets are subject to probate. Certain accounts and property types transfer automatically based on how they are titled or designated. For a full breakdown see: What Assets Don’t Go Through Probate in California?

A New Threshold, A Smarter Plan

This change opens the door to simpler, more efficient estate administration for many California families, but it also raises new planning questions that are worth getting right. Whether you are updating an existing plan or evaluating your options for the first time, understanding how the California small estate limit applies to your specific situation can make a meaningful difference in cost, timing, and overall control.

If you are ready to take the next step, reach out to Randal P. Hannah for guidance tailored to your goals. Give us a call or fill out our online form to schedule your free consultation.