TL;DR

Probate in California is often slower and more expensive than families expect, but it does not apply to every asset. In fact, many assets transfer automatically outside of court based on how they are titled or designated. Understanding which assets bypass probate is one of the most important parts of effective estate planning and efficient estate administration. A well-structured plan is designed to move as much as possible into these non-probate categories while maintaining control and clarity. In this guide, we will break down the main types of non-probate assets in California, how they transfer, and how they fit into a broader strategy to avoid probate in California wherever possible.

How Probate Works at a High Level

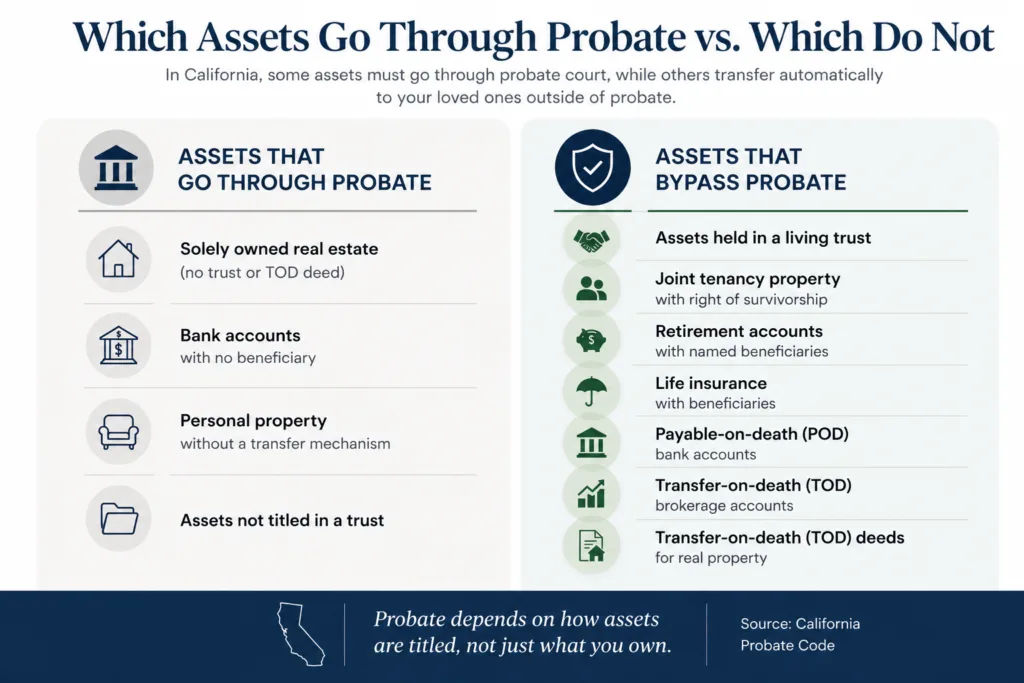

Probate is a court-supervised process used to transfer assets that were owned solely in the decedent’s name with no built-in transfer mechanism. If there is no trust, joint owner, or named beneficiary, the asset generally must go through probate. Assets with an existing transfer structure in place typically bypass probate entirely.

Assets Held in a Living Trust

Assets properly titled in the name of a revocable living trust pass through the successor trustee, not the probate court. This is one of the most reliable ways to avoid probate in California and maintain control over how assets are managed and distributed. However, simply creating a trust is not enough. The assets must actually be transferred into the trust. Failing to fund the trust is a common mistake that can result in those assets still being subject to probate.

Joint Tenancy and Tenancy by the Entirety

Real property and financial accounts held in joint tenancy with right of survivorship pass directly to the surviving owner without going through probate. Tenancy by the entirety, which is limited to married couples in certain contexts, offers a similar survivorship feature with added creditor protections. One limitation to keep in mind is that joint tenancy can affect potential community property tax basis advantages. For a deeper breakdown see our article on Community Property.

The Risks of Adding Children as Joint Owners

Many parents are told that adding an adult child to a bank account or deed as a joint tenant is an easy way to avoid probate. While this strategy may allow the asset to pass outside of probate, it also creates significant legal and financial risks that are often overlooked.

When a child is added as a joint tenant or co-owner, the child becomes a present owner of the asset, not merely a future beneficiary. As a result:

- The parent may not be able to sell, refinance, or transfer the property without the child’s cooperation and consent.

- The parent generally cannot remove the child’s ownership interest unilaterally.

- If the child lives in the property, disputes over possession and occupancy can become significantly more complicated.

- The child’s ownership interest may be exposed to the child’s creditors, lawsuits, bankruptcy proceedings, or divorce claims.

- The transfer may create gift tax reporting obligations and can eliminate valuable tax basis adjustments that might otherwise be available at death.

For these reasons, adding a child to title solely to avoid probate is often not the most effective estate planning strategy. In many situations, a properly funded living trust can accomplish the same probate-avoidance goal while allowing the parent to maintain full control of the asset during life.

Beneficiary-Designated Accounts

Assets with named beneficiaries pass directly to those individuals upon death. This includes retirement accounts such as 401(k)s and IRAs, life insurance policies, and annuities. These designations control the transfer regardless of what a will says, which is a critical detail many overlook when coordinating an estate plan.

Payable-on-Death and Transfer-on-Death Accounts

Bank accounts can be structured as payable-on-death (POD), and brokerage accounts can be set up as transfer-on-death (TOD), allowing assets to pass directly to a named beneficiary. California also permits transfer-on-death deeds for real property under California Probate Code § 5600 et seq. While these tools can be effective, they come with limitations, including revocability during life and potential exposure to disputes after death.

Community Property Passing to a Surviving Spouse

Community property passing to a surviving spouse can often be transferred using a Spousal Property Petition under Probate Code § 13500, avoiding full probate. This provides a more streamlined court process in many cases. For how property is classified and why it matters see: Community Property.

Small Estates Under the California Threshold

Certain estates may qualify for simplified procedures instead of full probate. Real property that qualifies under the updated threshold can use a streamlined petition process, and personal property under $208,850 may be transferred using a small estate affidavit. For a detailed breakdown of the updated California small estate limit and how it applies see: Small Estate Threshold.

Common Misconceptions

These issues come up often, especially when assets were set up at different times or without a coordinated plan. Clearing them up early can prevent unintended outcomes and unnecessary probate exposure.

- A will does not avoid probate. It directs how assets are handled within probate.

- Naming a beneficiary on an account overrides what a will says about that specific asset.

- A trust does not control assets that were never retitled into the trust’s name.

- Joint tenancy is convenient, but it is not always the most favorable tax structure for married couples.

- Adding an adult child to a deed as a joint tenant is treated as a present ownership transfer and can create significant tax, creditor, and control issues. While it may avoid probate, the child becomes an actual owner of the property, which can expose the asset to the child’s debts, legal claims, and consent rights.

Building a Probate-Free Estate Plan

The most reliable way to avoid probate in California is through a coordinated approach. A properly funded living trust serves as the foundation, supported by well-aligned beneficiary designations, strategic use of joint ownership where appropriate, and a pour-over will to capture anything unintentionally left outside the plan. When these pieces work together, assets transfer more efficiently and with far less court involvement.

If you want to build or review a plan that minimizes probate exposure while protecting your long-term goals, reach out to Randal P. Hannah Attorney at Law. You can schedule a free consultation by calling the office or using our online contact form.

Frequently Asked Questions

What assets are exempt from probate in California?

Assets that have a built-in transfer mechanism generally bypass probate. This includes assets held in a living trust, jointly owned property with right of survivorship, accounts with named beneficiaries, and payable-on-death or transfer-on-death accounts.

Does a living trust avoid probate in California?

Yes, if it is properly funded. Assets titled in the name of a living trust are managed and distributed by the successor trustee without going through probate. If assets were never transferred into the trust, they may still be subject to probate.

Do retirement accounts go through probate?

Typically, no. Retirement accounts such as 401(k)s and IRAs pass directly to the named beneficiaries. The beneficiary designation controls, even if the will says something different.

How do I avoid probate on real estate in California?

Common strategies include holding the property in a living trust, using joint tenancy with right of survivorship, or in some cases using a transfer-on-death deed. In certain situations, smaller estates may also qualify for a simplified court procedure instead of full probate.

Plan It Now, Avoid It Later

Avoiding probate in California is not about one tool, it is about how everything works together. The way your assets are titled, the beneficiaries you name, and whether your trust is properly funded all determine what happens when the time comes. A well-structured plan keeps transfers simple, reduces delays, and avoids unnecessary court involvement.

If you want to make sure your plan is set up the right way, connect with Randal P. Hannah. Call our office or schedule a free consultation through our online form.